If you're starting to budget for a new roof, the roof replacement cost in Florida can feel intimidating. Most homeowners spend between $11,000 and $30,000. That's a huge range, but it's driven by Florida's unique climate—from the punishing sun to the constant threat of hurricanes, every part of the job is affected. This guide provides actionable insights to help you navigate the process and make informed financial decisions.

The Real Cost of a New Roof in Florida

Thinking about a new roof in the Sunshine State isn’t just about picking out colors. It’s an investment in arming your home against everything from daily downpours to major storms. The final price tag isn't a random number; it's a careful calculation based on several key factors. Understanding these puts you in control of the conversation with contractors.

The biggest things that will move the needle on your estimate are the size of your roof, the materials you pick, and the strict building codes we have to follow here. For a typical 1,700 to 2,000-square-foot home, you can expect the average to be around $15,000. But remember, that number can swing wildly depending on your specific situation. You can explore more about this cost breakdown and its contributing factors to see how different choices add up.

Key Cost Influencers at a Glance

So, what exactly are contractors looking at when they write up your quote? Let's break down the main pieces of the puzzle. Each one plays a part in the total investment needed to keep your home safe and sound.

A new roof in Florida isn't just another home repair—it's an investment in resilience. Those strict building codes might add to the initial cost, but they're there for a reason: to make sure your home can stand up to hurricane-force winds and give you real peace of mind.

To give you a clearer picture, this table sums up the major cost drivers. It shows what affects the price and, more importantly, why it matters so much in our demanding Florida climate. Use this as your cheat sheet for understanding any estimate that comes your way.

Key Factors Influencing Your Florida Roof Replacement Cost

| Cost Factor | Average Impact on Price | Why It Matters in Florida |

|---|---|---|

| Roof Size & Complexity | High | A bigger or steeper roof needs more materials and more skilled labor, which directly drives up the cost. Simple as that. |

| Roofing Material | High | Your choice, from budget-friendly asphalt shingles to premium metal or tile, is one of the biggest factors in the final price. |

| Florida Building Codes | Medium | Things like a secondary water barrier and specific nailing patterns are required by law, adding to both material and labor costs. |

Getting a handle on these variables is the first step. It helps you see where your money is going and allows you to have a much more productive conversation with your roofing contractor about your options.

How Contractors Calculate Your Roofing Estimate

When a roofing contractor hands you an estimate, that final number isn't just pulled out of thin air. It’s a detailed calculation built on one core metric: the cost per square foot. Think of this as the price for every single 10-foot by 10-foot square of your roof. It's the building block for your entire project budget.

Actionable Insight: Don't just look at the total price on a quote. Ask every contractor for their cost-per-square-foot breakdown. This allows you to compare bids on an apples-to-apples basis and question any major differences. A transparent, trustworthy contractor should be able to walk you through exactly how they landed on their rate.

Looking at the numbers for a roof replacement in Florida, you'll see prices that typically range from $4.35 to $11 per square foot, all depending on the specific details of the job. For a standard 1,000 to 2,000-square-foot home, this means the total cost can swing from $4,350 to well over $33,000. You can get a much deeper understanding of these Florida-specific roofing cost factors and how they influence prices to see where your project might land.

The Power of the Per-Square-Foot Rate

It might seem like a minor detail, but even a small difference in the per-square-foot rate has a huge impact on your total roof replacement cost in Florida. The cost multiplies quickly over the entire surface area of your roof.

Let’s put it into perspective with a real-world example. Say you have a 2,000-square-foot roof.

- Contractor A quotes $6.00 per square foot, which comes out to a $12,000 total.

- Contractor B quotes $7.50 per square foot, for a final price of $15,000.

That seemingly small $1.50 difference per square foot just created a $3,000 gap in the final quotes. This is exactly why you need to look past the bottom-line price and ask contractors to break down their costs. It’s the only way to compare quotes fairly and see where your money is really going.

Understanding the cost per square foot is like knowing the price per gallon of gas before you fill up your car. It empowers you to make a smart decision and ensures you're getting fair value for a major investment in your home.

This all-important number isn't arbitrary. It’s a carefully calculated figure that bundles together several key parts of the job. A professional estimate will always account for the unique challenges and requirements of your specific roof.

What Drives the Cost Per Square Foot

So, what goes into that number? Three main factors determine your specific per-square-foot rate. Each one represents a different piece of the puzzle—labor, materials, and the safety measures needed to build a roof that can stand up to the Florida climate.

Roof Pitch and Complexity: "Pitch" is just the roofer's term for your roof's steepness. A low-slope or nearly flat roof is much easier and safer for a crew to work on, which keeps labor costs down. On the other hand, a steep, complex roof with lots of gables, valleys, and dormers requires more time, specialized safety gear, and a higher level of skill, which drives up the price.

Tear-Off Labor: In almost all cases, Florida building codes demand a full tear-off of the old roofing materials. This isn't just about hauling away debris; it’s a critical step that lets the crew inspect the underlying roof deck for damage. The labor to strip every old shingle, dispose of the waste, and get the surface ready for the new roof is a significant part of the upfront cost.

Underlayment and Water Barriers: Here in Florida, the underlayment isn't just a simple layer of felt paper. State codes mandate a secondary water barrier, which is usually a "peel-and-stick" membrane that seals directly to the roof deck. It’s a game-changer, providing a vital second line of defense against leaks if you lose shingles in a hurricane. This superior protection, however, adds to both material and labor costs.

Choosing the Right Roofing Material for Florida

When it comes to your roof replacement cost in Florida, the single biggest decision you'll make is the material you choose. This isn't just about curb appeal; it's a critical investment in your home's defense against our state's unique challenges—the blistering sun, relentless downpours, and, of course, hurricane-force winds. The right material doesn't just keep you dry; it can even affect your insurance premiums.

Let's move past just the price tags. We're going to break down the top materials through the eyes of a Florida homeowner, giving you the real-world insight you need to make a smart financial decision. We'll look at the big three: asphalt shingles, metal, and tile.

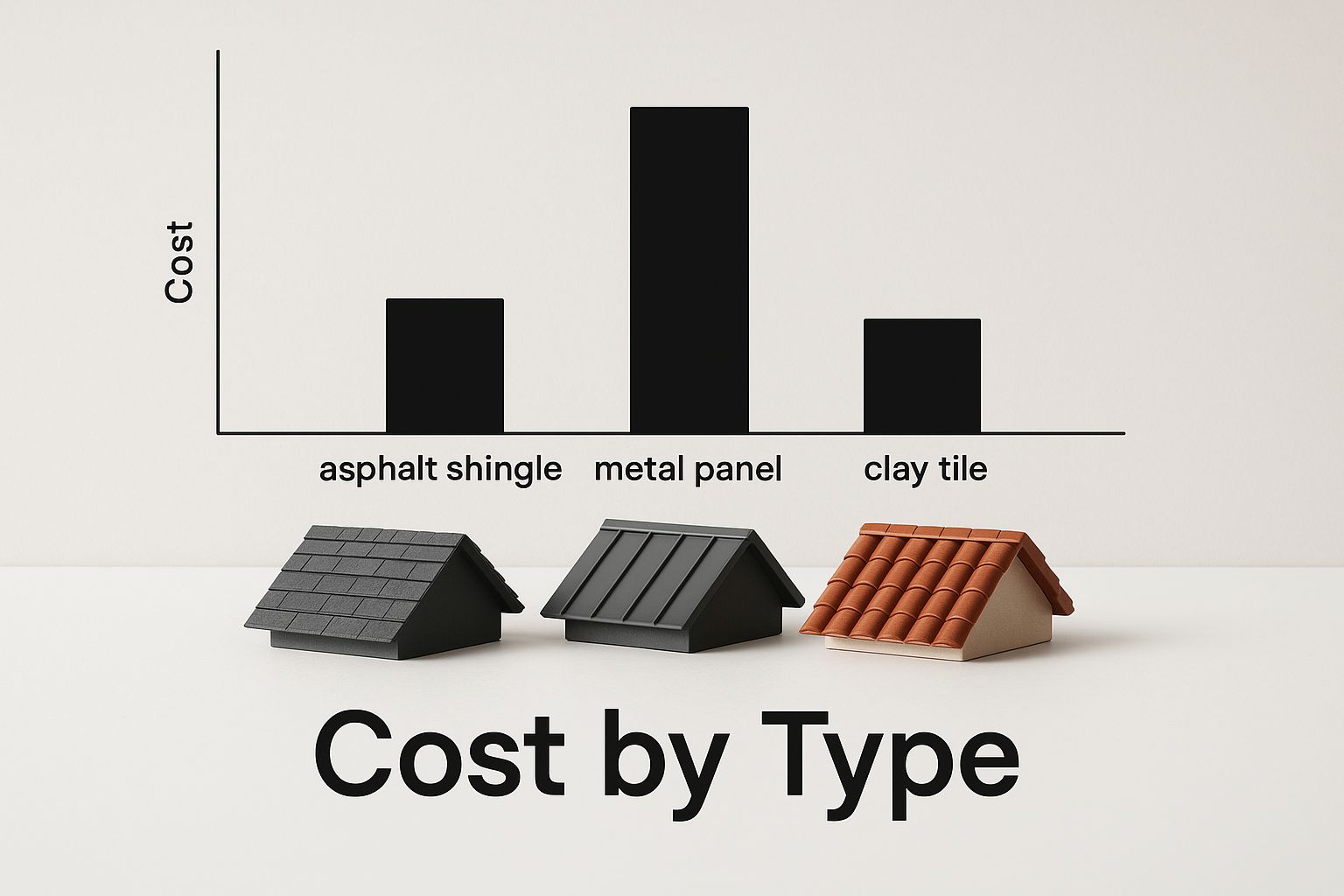

This quick visual gives you a high-level look at how these materials stack up on cost.

As you can see, there’s a clear step-up in cost from shingles to metal and then tile. This progression isn't arbitrary; it directly reflects how long each material is expected to last and how well it stands up to mother nature.

Asphalt Shingles: The Popular and Practical Choice

Asphalt shingles are the most common choice in Florida because they are the most affordable upfront. For homeowners working with a tight budget, shingles offer a classic look that suits just about any style of home.

However, that lower initial cost comes with a shorter lifespan here. In Florida’s harsh climate, a standard asphalt shingle roof has a realistic lifespan of 15-20 years. That's a far cry from the 30-year warranties you might see advertised for homes in milder parts of the country. While they can handle typical weather, they are the most vulnerable to damage from hurricane-force winds.

Actionable Insight: If you choose shingles, opt for "architectural" or "dimensional" shingles. They are thicker, more wind-resistant, and have a more premium look than basic 3-tab shingles for a marginal increase in cost.

Metal Roofing: The Durable and Resilient Contender

Metal roofing has exploded in popularity across Florida, and it all comes down to one word: resilience. Yes, the upfront investment is higher than shingles, but a metal roof can last 40 to 70 years. For many, it's a "one-and-done" roofing solution. They are exceptionally tough against high winds, moisture, and fire.

In fact, Florida’s own Insurance Commissioner has suggested the state should look at phasing out less durable materials. The push is toward more resilient options like metal to make our homes more insurable and reduce the massive damage we see after storms. This shows you just how much long-term value state officials and insurance companies see in stronger roofs.

On top of its strength, metal is also incredibly energy-efficient. The reflective surface bounces solar heat away from your home, which can lead to noticeable savings on your cooling bills during our long, sweltering summers. The main downsides? The higher initial cost and the fact that some people find them a bit louder during a heavy rainstorm.

Tile Roofing: The Premium and Timeless Option

Made from clay or concrete, tile is the undisputed heavyweight champion of Florida roofing. It delivers a timeless, high-end look and durability that’s second to none, with a lifespan that can easily exceed 50 years if properly maintained.

Tiles are practically immune to fire, rot, and insects. Their immense weight and interlocking design create a formidable shield against hurricane-force winds, which is why you see them so often in upscale coastal communities.

Of course, this top-tier performance comes with a premium price tag. Tile is one of the most expensive materials, and its sheer weight means your home's structure has to be engineered to support it. But for homeowners who value longevity and aesthetics above all, a tile roof is an incredible investment that pays off in both protection and property value.

As you explore these options, using a construction material cost predictor can be a helpful tool for getting a ballpark idea of material expenses.

Florida Roofing Material Comparison

To make things easier, we’ve put the key details side-by-side. Use this table to compare the trade-offs between what you pay now, how long the roof will last, and how it will perform when a big storm hits.

| Material | Average Cost per Sq. Foot (Installed) | Typical Lifespan in Florida | Hurricane Resistance |

|---|---|---|---|

| Asphalt Shingles | $5.50 – $7.50 | 15-20 Years | Good |

| Metal | $9.50 – $15.50 | 40-70 Years | Excellent |

| Tile (Clay/Concrete) | $12.00 – $15.00+ | 50+ Years | Excellent |

Ultimately, choosing the right material comes down to balancing your immediate budget with your long-term goals for your home’s safety, value, and peace of mind.

Decoding Labor Costs and Choosing Your Contractor

It’s easy to focus on materials, but the skill, sweat, and expertise of the roofing crew frequently makes up more than half of your total bill. This part of the roof replacement cost in Florida is about so much more than just nailing down shingles.

You're paying for a tough, multi-step job. It starts with the careful tear-off of your old roof, followed by a detailed inspection of the underlying deck. Then comes the precision installation that must meet Florida's notoriously strict building codes, and finally, a complete site cleanup. It’s physically demanding work that requires real skill.

Understanding what drives this cost is key. For example, a steep, complex roof loaded with dormers and valleys is a whole different ballgame than a simple, low-pitch gable roof. The crew needs more time, specialized safety gear, and a higher level of precision for those tricky designs, and that's going to show up in the final price.

What Is a Fair Labor Rate in Florida?

While rates will always vary a bit by city and a contractor's reputation, it helps to know the ballpark. The demand for good roofers in Florida is intense, with the state employing around 25,190 roofing professionals.

These are skilled tradespeople earning a solid wage, averaging about $22.61 per hour, which works out to a median annual salary near $47,000. Knowing this gives you context for the labor charges on your quote. They aren't just random numbers; they reflect real-world wages for a demanding job. You can read the full analysis on roofing employment trends to see how Florida's market stacks up.

Think of hiring a roofer like hiring a surgeon for your home. You're not just paying for their time; you're investing in their experience, precision, and ability to protect your most valuable asset from the elements. The cheapest option is rarely the best value.

A quality contractor's labor cost doesn't just cover wages. It also includes essentials like insurance, warranties, and the project management needed to keep everything on track. Trying to save a buck on labor is one of the biggest gambles you can take, and it often leads to leaks, failed inspections, and much more expensive repairs later on.

Your Actionable Contractor Vetting Checklist

Choosing the right contractor is the most critical decision you'll make. A great roofer delivers a high-quality, long-lasting installation. A bad one can turn your project into an absolute nightmare. Use this checklist to screen every potential contractor like a pro.

1. Verify License and Insurance Instantly

Don't just take their word for it. Every legitimate Florida roofer must hold a state-issued license and carry both general liability and worker's compensation insurance. No exceptions.

- Actionable Step: Ask for their license number and the name of their insurance carrier. You can easily verify a Florida contractor's license online. The insurance is what protects you from any liability if a worker gets hurt on your property.

2. Ask for a Local and Recent Reference List

Any contractor worth their salt will be proud of their work and happy to share it. Ask for a list of recent jobs they've completed right in your area.

- Actionable Step: Don't just get the list—actually call a few of them. Ask about their overall experience, if the project stayed on budget, and how well the crew cleaned up after themselves.

3. Demand a Detailed, Written Contract

A handshake deal or a vague, one-page quote is a massive red flag. A professional, detailed contract is your single best defense against surprise costs and future arguments.

- Actionable Step: Make sure the contract spells out the full scope of work, the specific materials to be used (down to the brand names), a clear payment schedule, estimated start and finish dates, and all warranty details. Never, ever sign a contract with blank spaces.

4. Inquire About Their Warranty

You should get two types of warranties: one from the material manufacturer and another from the contractor covering their workmanship.

- Actionable Step: Get the details on both. A solid workmanship warranty (typically 5-10 years) shows the contractor truly stands behind their installation quality. That’s the kind of confidence you want for long-term peace of mind.

How Florida Building Codes Impact Your Wallet

Here in Florida, building codes aren't just annoying red tape. They're a direct result of our state’s wild weather, born from the lessons learned after every major hurricane. Think of them as a mandatory armor upgrade for your home.

These rules absolutely influence your roof replacement cost in Florida, but they also seriously beef up your home's defenses. It's a trade-off that pays you back in safety and priceless peace of mind.

These regulations are the law. They are strict, non-negotiable requirements every licensed contractor must follow perfectly. Cutting corners doesn't just mean a failed inspection; it means your home is left wide open to the next big storm. Understanding why these codes exist helps you see exactly where your money is going and appreciate the protection you’re buying.

Non-Negotiable Hurricane-Proofing Measures

When a roofer hands you an estimate, a good chunk of that cost goes toward meeting the Florida Building Code—and for good reason. It's one of the toughest in the country. After every storm season, experts figure out what held up and what blew away, and those lessons get written directly into the code.

Here are the key requirements that will be part of your roofing project:

- Complete Tear-Off: Forget about layering new shingles over old ones. The code almost always demands a full tear-off right down to the wooden roof deck. This is critical because it lets the crew inspect the deck for any rot or damage and ensures a solid foundation for your new roof.

- Roof Deck Nailing: That plywood deck has to be fastened with a very specific nailing pattern. The code tells us the exact type, size, and spacing of the nails to keep the deck from getting ripped off by hurricane-force winds.

- Secondary Water Barrier: This might be the single most important upgrade. We install a self-adhering membrane, commonly called "peel-and-stick" underlayment, right onto the roof deck. If shingles get blown off in a storm, this sealed barrier is your last line of defense against a catastrophic leak.

Yes, these upgrades add to the initial cost of a new roof. But they are absolutely essential. A roof that isn't built to code is a gamble no Florida homeowner can afford to take.

Turning Code Compliance into Insurance Savings

Now for the good part. A new, code-compliant roof isn't just an expense—it's one of your best tools for slashing your homeowners insurance premiums. Why? Because insurance companies give major discounts for homes that are less likely to suffer wind damage.

A new roof built to today's stringent codes is one of the single most effective things you can do to lower your insurance bill. You are proactively reducing the insurance company's risk, and they will reward you for it.

The secret to cashing in on these savings is the wind mitigation inspection. This is a special inspection done by a certified pro right after your new roof is finished. The inspector's job is to officially document all the hurricane-resistant features your roofer just installed.

Your Action Plan for Lower Premiums

Don't miss out on this. Turning your new roof into real savings just takes a few simple steps. This process puts you in the driver's seat, letting you turn your home's new strength into a direct financial win.

- Schedule the Inspection: As soon as our crew packs up, call a certified wind mitigation inspector. We can always recommend a good one.

- Get the Report: The inspector will give you an official report (Form OIR-B1-1802). It details everything about your new roof: its age, how the deck is attached, the water barrier, and more.

- Submit to Your Insurer: Send that report to your insurance agent immediately. They'll use that proof to apply every single discount you're entitled to.

The savings can be huge—often hundreds, sometimes even thousands of dollars a year. By doing this, you make the building code work for you, turning a necessary expense into a smart, long-term financial move.

Smart Ways to Budget and Pay for Your New Roof

Staring down a major home project like a new roof can feel daunting, but having a solid game plan for your money can turn that stress into confidence. The high roof replacement cost in Florida is a reality, but it doesn't have to be a roadblock. With a clear budget and a good handle on your payment options, you can tackle this project head-on.

Actionable Insight: Build a contingency fund of 10-15% of the total project cost into your budget from the start. If your quotes average $15,000, plan for at least an extra $1,500. This buffer is your safety net for unexpected issues, like discovering rotted decking after the old roof comes off. A professional contractor should discuss this possibility with you upfront.

Common Ways to Fund Your Florida Roof Replacement

Once you've got a budget in mind, the next question is how to pay for it. The good news is that Florida homeowners have several solid options. It's all about finding the one that fits your financial comfort zone.

- Home Equity Line of Credit (HELOC): This is basically a credit card that’s secured by your home's equity. You draw funds as you go, which is perfect for a big project where the final cost might shift a bit.

- Personal Loans: If you prefer predictability, an unsecured personal loan from a bank or credit union is a great choice. You get a lump sum upfront and have a fixed interest rate with regular monthly payments. No surprises.

- Contractor Financing: Many roofing companies, including ours, partner with lenders to offer financing directly. It can be a convenient, all-in-one solution, but you should always compare the interest rates to what your own bank can offer.

And if your roof was damaged in a storm, your insurance company will be a big part of this conversation. Successfully navigating the home insurance claim process is absolutely key to getting a fair and smooth payout. Make sure you understand your policy and document everything.

Protecting Your Investment

A huge part of budgeting is understanding how you'll pay and spotting the red flags that could end up costing you big time. A professional contractor has a payment schedule that protects both of you.

A reputable roofer will never demand the full amount in cash upfront. A large upfront payment demand is the biggest red flag in the industry. Legitimate payment schedules align with project milestones, ensuring you only pay for work as it's completed.

A typical, safe payment schedule should look something like this:

- Initial Deposit: A small percentage, usually around 10%, when you sign the contract.

- Materials Delivery: A larger payment, say 40%, once the materials are delivered to your property.

- Project Completion: The final balance of 50% is paid only after the job is done, the site is clean, and you've given it your final nod of approval.

Finally, always ask about potential savings! Choosing energy-efficient materials or impact-resistant shingles that meet Florida's tough wind mitigation standards might make you eligible for tax credits or rebates from the manufacturer, which can help bring down the overall cost.

Common Questions About Florida Roof Replacement Costs

Even after you've weighed the materials and considered the building codes, a few questions are bound to pop up. We get it. Here are some straight answers to the most common things Florida homeowners ask, so you can move forward with your roof replacement feeling completely confident.

How Often Should a Roof Be Replaced in Florida?

The lifespan of your roof is all about the material it's made from. For asphalt shingles, the most common choice, you're looking at about 15-20 years in Florida. That might seem short, especially when you see 30-year warranties, but our intense sun and storm season really take a toll.

Want something that lasts longer? A well-installed metal roof can protect your home for 40-70 years, while a high-quality tile roof can easily last 50 years or more. The key, no matter the material, is to get annual inspections. That’s how you spot small issues before they turn into major, expensive problems.

Can I Install a New Roof Over an Old One?

Here in Florida, the answer is a hard no. Our state building codes are very strict on this and almost always demand a complete tear-off of the old roof, right down to the wood deck.

This isn’t just the state being difficult. It’s an essential safety step. A full tear-off is the only way for your contractor to properly inspect the underlying deck for any rot, water damage, or weak spots. Making sure that foundation is solid is non-negotiable for ensuring your new roof can stand up to hurricane-force winds.

A complete tear-off is mandatory because it’s the only way to verify the structural integrity of your roof deck. Layering new materials over old ones can hide serious problems and compromise the entire roofing system's ability to protect your home.

Does Homeowners Insurance Cover a Full Replacement?

Whether insurance foots the bill depends entirely on your policy and why you need a new roof. If a specific, covered event like a hurricane or a major storm damages your roof, your policy will likely pay for the replacement (minus your deductible, of course).

But here’s the crucial part: insurance will not pay to replace a roof just because it’s old. It’s vital to know that many Florida insurance carriers are now limiting coverage based on a roof’s age. Instead of paying the full replacement cost for an older roof, they may only offer its depreciated "actual cash value."

What Is a Wind Mitigation Inspection?

Think of a wind mitigation inspection as your new roof’s final report card. After your code-compliant roof is installed, a certified inspector comes out to document all its hurricane-ready features—like the stronger nailing patterns and the secondary water barrier.

This official report proves to your insurance company that your home is better protected against wind damage. The result? You can earn significant discounts on your homeowners insurance premiums. It’s an essential final step that turns a necessary expense into a smart, long-term investment.

Ready to get a clear, no-nonsense estimate for your South Florida roof replacement? The experts at Exact Roofing provide detailed inspections and transparent quotes to ensure you get the best value and protection for your home. Visit us at https://www.exactcontractors.com to schedule your free consultation today.

Article created using Outrank